It’s fairly common for manga or light novels getting an anime adaptation to receive some sort of boost in sales after the anime airs. However, both the presence or size of those bumps varies widely. These bumps represent an interesting opportunity for study, since they represent (potentially) an alternative indicator of both the financial impact of anime, as well as a look at the broader-scale demand curve for franchise-related goods. Not everybody can or will easily pay 30,000 yen for a full special-feature-laden set of disks, but such casual fans could still have a big impact on a series if the manga is within their price range.

The real fascinating part of this, though, is that casual fans need not support at all. While one almost certainly has to watch a show to be willing to buy the disks or even the manga, the reverse need not apply. The fact that the relation between disk averages and print boosts is so fragmentary implies a potentially similar disconnect between print bumps and total interest generated by a show.

In theory, sales should be better represented by casual indicators of popularity as costs get lower. In practice, the statistics are pretty garbled, though they do offer a hint as to which sorts of series may end up with bumps at the end of the day. To attempt to better understand the junk described above, I broke down 4 categories potentially indicating no-cost and low-cost popularity, and compared their ratings with the print-bump successes of series which got anime adaptations in Summer and Fall of 2013. Note that while I originally used Torne rankings in the earlier analyses, I discarded the data because of how incomplete they were.

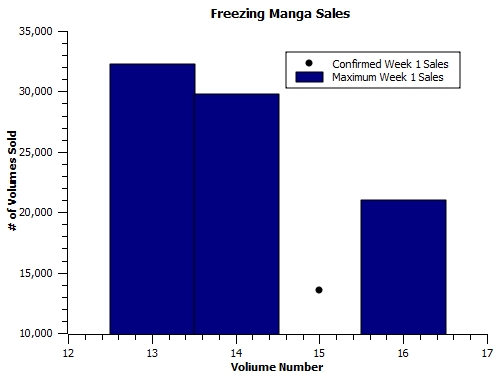

For the purposes of this article, a “significant boost” is one where a series experiences a 20% jump in sales or charts for the first time after the anime. All figures are for a volume’s first 2 weeks of sales, calculated with the average of the 2 most immediate before and after volumes, if 2 volumes of data are available in each case. Be aware that this is not a comprehensive measure of which series got boosts, just one intended to at least catch the biggest ones. 1/3 of all series got such a visible bump, meaning the null-hypothesis accuracy rate these indicators need to beat is 66.6%~67%.

In addition to the previous top 5/10/15 tests used for v1 disk sales, I’ve also included histograms of how successful series were scattered across the indicator. Ideally, they would all be 60th percentile or better, but reality isn’t quite that nice.